The following was posted by Bill Mitchell, Professor in Economics and Director of the Centre of Full Employment and Equity (CofFEE), at the University of Newcastle, NSW, appeared on 28 August 2017 on Billy Blog.

The latest report from the Australian Council of Superannuation Investors released on Thursday (August 24, 2017) – CEO Pay in ASX200 Companies: 2016 – shows how unfair and unsustainable the income distribution is in Australia. While there has been moderation in the growth of CEO pay after the ‘greed is good’ binge leading up to the GFC, the managerial class in Australia has still enjoyed real growth in pay at a time when the average worker is enduring either flat to negative growth in pay.

Further, overall economic growth in Australia is being driven by increased non-government indebtedness as real wages growth (what there is of it) lags well behind productivity growth. And, at the same time, the Federal Government is intent on pursuing an austerity policy stance. All these trends are similar to the dynamics we experienced in the lead-up to the GFC. They are unsustainable. A major shift in income distribution away from capital towards workers has to occur before a sustainable future is achieved. The indicators are that there is no pressure for that to occur.

Late last week it was disclosed that the out-going Australia Post (a state-owned company) was given a departing payment of $A10.8 million which included $A8.7 million in bonuses on top of his base salary of $A2.04 million per year.

The state secretary of the Communications Workers Union, which covers Australia Post workers responded with:

… It is obscene that Ahmed Fahour is walking away with nearly $11 million as a pay-off for slashing the postal services of all Australians. Our members, who are receiving a less than CPI [inflation] pay rise, are absolutely outraged.

When his base salary was disclosed earlier in the year, the public outrage was so great that the CEO was forced to resign, although they massaged this as being a natural transition.

This was similar to the recent announcement surrounding the announcement that the CEO of the privatised public bank – Commonwealth Bank of Australia – was resigning, not long after the Bank was charged with 53,700 contraventions of Australia’s money laundering and terrorism laws.

The Authority charged with maintaining the integrity of transactions (AUSTRAC) has said that the CBA failed to report a massive number of suspicious transactions (Source).

That was the latest in the sequence of scandals the CBA has been involved in as it chases profits without regard to workers, customers and, it seems, probity.

And today there was news (August 28, 2017) – Commonwealth Bank facing APRA probe – that the Australian Prudential Regulation Authority (APRA) has announced an:

… inquiry into the Commonwealth Bank’s culture, governance, and accountability systems, prompted by a run of run of scandals at the country’s largest lender.

They cited a public distrust for the CBA after a series of obvious failures at the highest level of the bank.

The Australia Post CEO received the ridiculously-large bonuses for doing things like pushing through increases in stamp prices (from 70 cents to $A1) and forcing workers into six-day deliveries. Priorities!

The Australia Post board tried to claim they had to pay this salary/bonus level to attract the right talent. Two questions arise:

- Why is the incoming CEO going to be paid “$1.375 million a year, with the potential to earn 100 per cent of that as a bonus”? (Source).

- Why are similar executives in the US paid on average $US230,090 per year (2016) if $A10 million or so is required to attract talent (Source)?

As noted in the Introduction, the Australian Council of Superannuation Investors published its latest annual CEO pay survey last Thursday (August 24, 2017) – CEO Pay in ASX200 Companies: 2016.

It covers executive pay for the 200 listed companies on the Australian Stock Exchange.

The survey shows that in 2001 (when the first survey was taken) the ratio of average CEO pay to total earnings by workers was 76 to 1. By 2016 this ratio was 85 to 1, although it peaked at 123 to 1 in 2007 just before the crisis.

I have already discussed on several occasions the widening gap between productivity growth and real wages growth, which manifests as an increasing profit share in national income and a decreasing wage share.

This redistribution of national income towards capital has been ongoing for the last three decades or so in most countries and is a characteristic of the neo-liberal era.

Where does the real income that the workers lose by being unable to gain real wages growth in line with productivity growth go?

Answer: Some of the redistributed income has been retained by firms and invested in financial markets fuelling the speculative bubbles around the world.

But some of the redistributed income has gone into paying the massive and obscene executive salaries that we are discussing in this blog.

For workers, the problem is that they rely on real wages growth to fund consumption growth and without it they borrow or the economy goes into recession. The former is what happened around the world in the lead up to the crisis (and caused the crisis).

The latter is more or less what is happening now.

One of the essential changes that needs to happen to ensure that another bout of financial instability doesn’t hit soon is that real wages have to grow in proportion with productivity growth – exactly the reverse of what is happening now.

That will require a fundamental revision of the way executive pay is determined and significantly reduced payout outcomes for the bosses.

The latest Australian data from the Australian Council of Superannuation Investors (ACSI), the body that “provides independent research and advice to assist its member superannuation funds to manage environmental, social and corporate governance (ESG) investment risk”, shows that:

– Almost one third of ASX100 CEOs (25 of 83) received bonuses equal to 80%, or more, of their potential maximum payout … executive bonuses in large companies are better described as “variable fixed pay”, rather than genuinely at-risk performance pay.

– Bonus persistence remained a feature in FY16 for ASX100 CEOs.

– The median bonus accrued for an ASX101-200 CEO rose almost 30% to $486,000 …

– Median … ASX100 CEO fixed pay … rose … 4.4% …

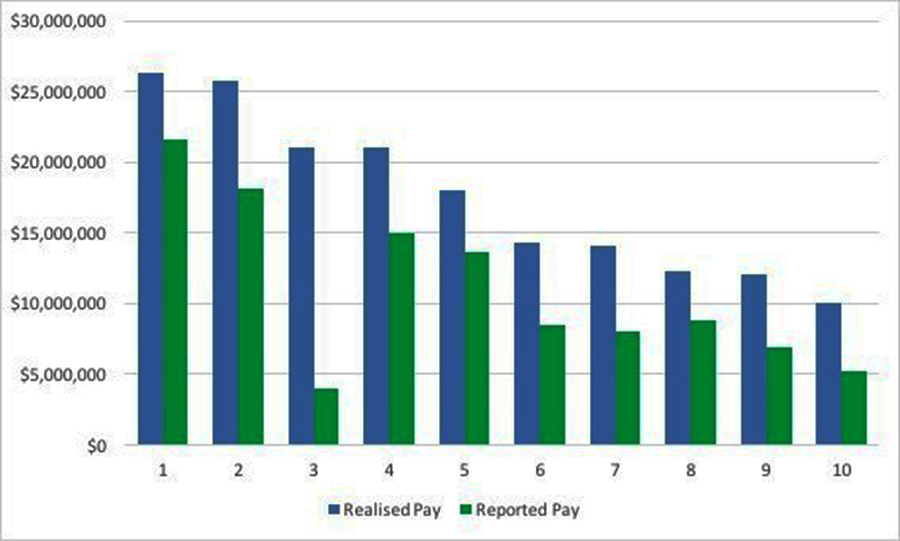

– Average realised pay (cash payments plus the value of vested equity) was again significantly higher than average reported pay …

The following graph shows the gap between the reported pay and realised pay for the top 10 CEO earners. It is clear that there is a significant variation in what the companies report in their Annual Reports and the extra payments associated with cash payments on top.

The ACSI had argued in an earlier Report that:

The ACSI had argued in an earlier Report that:

These figures suggest that the existing requirements for reporting executive pay may significantly understate the rewards received in a given year. Statutory reporting is, perhaps, disclosing only the tip of the iceberg in terms of the wealth accruing to senior executives …

In its current report, ACSI say that:

The prevalence of CEO bonuses at consistently high levels raises serious questions about the way performance hurdles are being designed and applied. The fact that only 18 CEOs received bonuses below 50% of maximum indicates that they bear little relation to performance in many companies.

Which goes to heart of the justifications given out by boards of these companies that they have to pay the high salaries to get the best to do the best.

In fact, these exorbitant bonuses which come out of incomes redistributed from workers and the price gouging these companies engage in, “bear little relation to performance in many companies”.

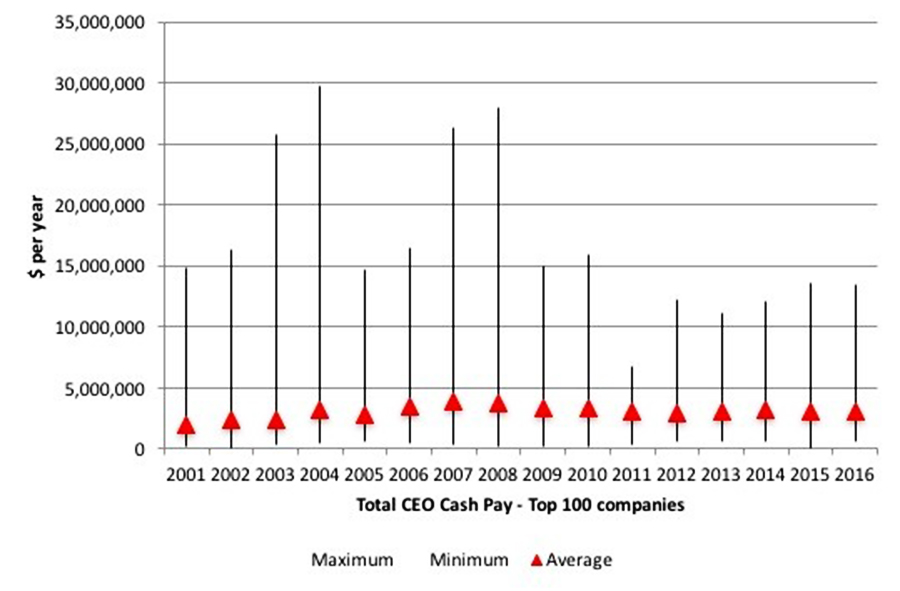

The next graph shows the average total CEO Cash Pay in the Top 100 companies (red triangles) and the maximum and minimum values for each year (indicated by the vertical lines).

The ACSI define the total cash pay as “fixed pay, cash bonuses and accrual of entitlements”, so more or less what an average worker might receive each year (the bonuses if they are lucky).

There is considerable disparity within the ranks of the CEOs (from max to min). There are some sensationally large salaries and some rather modest ones (in relative terms).

The next graph shows the average total CEO Statutory Pay in the Top 100 companies (red triangles) and the maximum and minimum values for each year (see accompanying table for actual dollar values).

The ACSI define statutory pay as “the total remuneration disclosed for a CEO in a company’s remuneration report, as required by Australian law. It therefore includes the value of share-based payments expensed under accounting standards”.

Don’t be fooled by the different scale of the axes in each graph – the statutory pay is a huge step up on the total cash pay although clearly well below the ultimate realised earnings (as detailed in the first graph).

Comparisons with other workers

But all of that analysis doesn’t mean much unless there is some context.

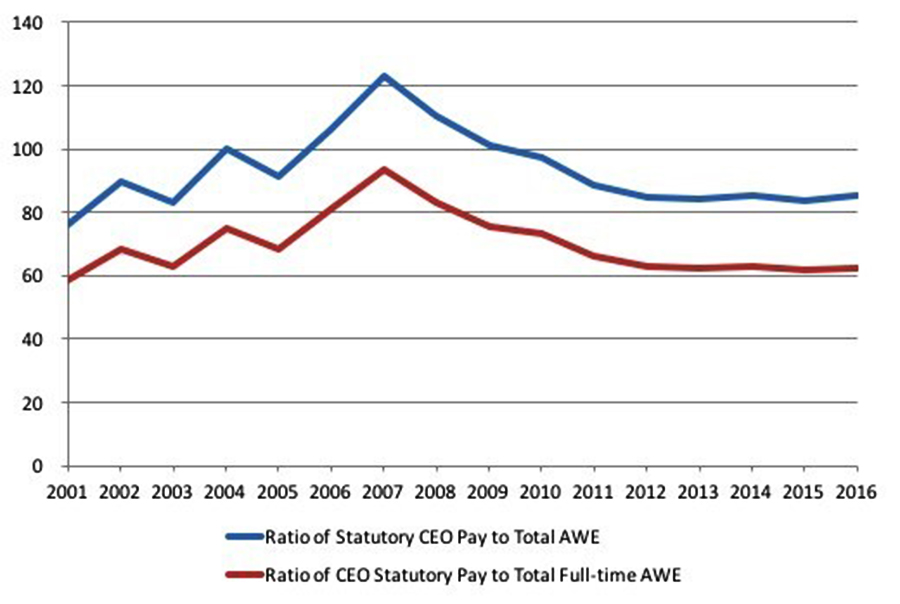

The next graph shows the Ratio of CEO Statutory Pay to Total Average Weekly Earnings (blue line) and Total Average Weekly Full-time Earnings (red line) from 2001 to 2014.

The ratio for the former started at 76.2 in 2001, peaked at 123.1 in 2007 at the height of the ‘greed is good’ frenzy and is now back to 85.2 and is rising again.

The ratio for the latter started at 58.6 in 2001, peaked at 93.7 in 2007 and is now back to 62.5 but it is also rising again.

These differentials are always justified by the conservatives and the business lobby as being essential to attract top quality executives. But then we know that company performance is not closely linked at times to the pay that the CEOs get, which puts a hole in that argument.

When the 2013 data was released on September 18, 2014, an accompanying press report – Pay for Australian CEOs is down, but it’s still too high said:

The boom that lit the fuse of the global crisis then overwhelmed commonsense and decency … Pay was out of control at that time in almost every way. Short-term bonus hurdles were too low, shares were vesting too quickly and on terms that were too generous, and termination payments were too big.

Company leaders offered various excuses, all of them lame.

This is the ‘greed is good’ frenzy that was associated with the total failure of the financial market and associated labour markets to self-regulate along the lines that the mainstream economics and finance textbooks claimed.

The UK-based High Pay Centre released its own study with CIPD earlier this month (August 3, 2017) – CIPD/High Pay Centre survey of FTSE100 CEO pay packages 2016 – which showed that several CEOs received pay rises despite major failings in their companies.

For example:

Mark Cutifani, CEO of Anglo-Americans, saw his pay package rise by half a million to £4.0 million despite the number

of fatalities among the workforce increasing to 11 fatalities, compared with six last year.

At BHP plc, the CEO received no short-term incentive because of the collapse of the Samarco dam.

One notable jump in CEO remuneration was Arnold Donald’s of Carnival plc. He earned just over £22 million in 2016 (from £6 million in 2015), the year in which Carnival was ordered to pay £32 million in penalty charges relating to its deliberate pollution of the seas and intentional acts to cover it up. This is the largest-ever criminal penalty involving deliberate vessel pollution.

This reinforces earlier work by CIPD report in Britain that has found the idea that CEO salaries a market determined is ridiculous. There is very limited scrutiny by shareholders, and company boards are bullied or cajoled by celebrity CEOs who reward compliance with personal gain.

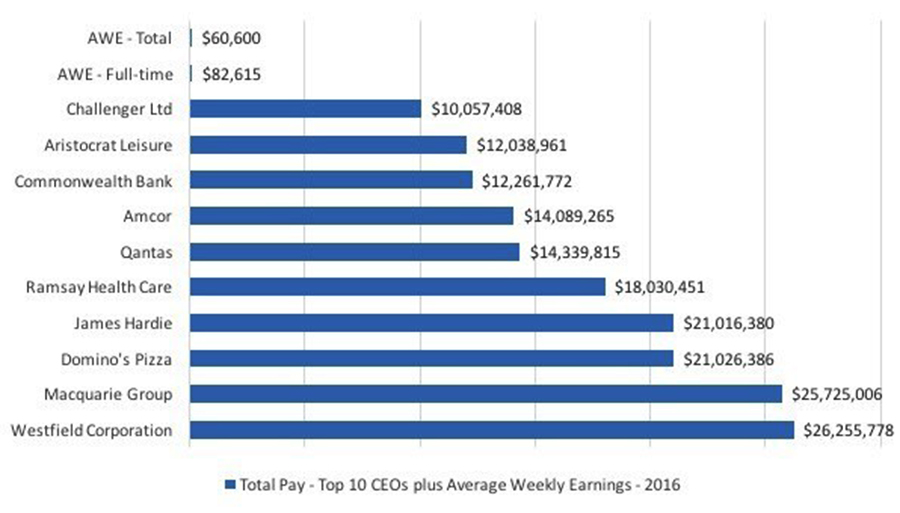

The next graph shows the salaries of the Top 10 CEOs in Australia compared to Average Weekly Earnings (Full-time) and Average Weekly Earnings (Total) for 2016.

The question is what does a person who runs a shopping centre empire contribute to society that is worth more than $A26 million a year relative to what an average worker contributes who only gets $A60,600 per year?

The question is unanswerable using any logic that is based on societal well-being, fairness, or decency.

The next graph shows the pay ratios of the Top 10 CEOs in Australia compared to Average Weekly Earnings (Full-time).

I have reported elsewhere that the growth in the Wage Price Index in Australia is at record lows (for several successive quarters).

Please read my blog – Australia – real wages growth zero and the rip-off of workers continues – for more discussion on this point.

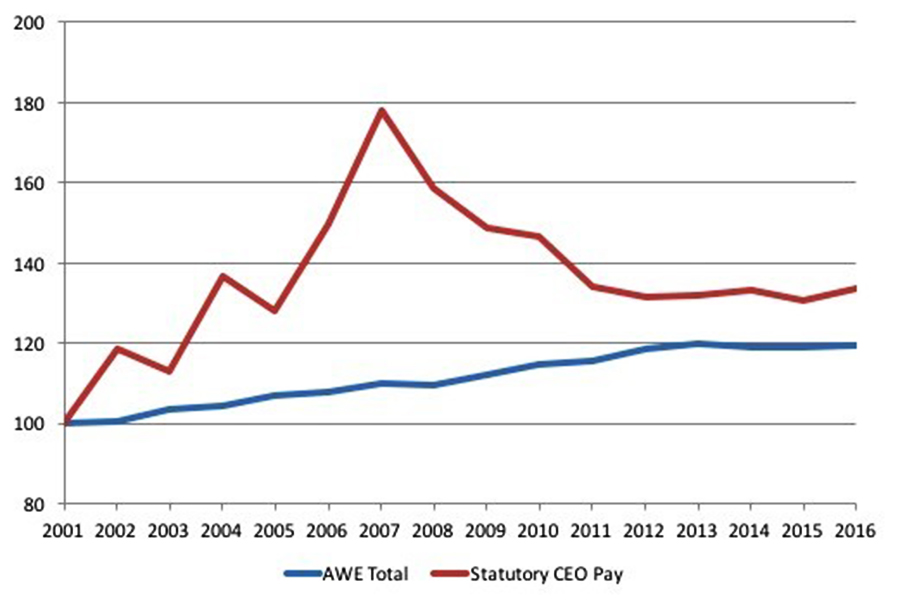

The following graph shows the movement in Average Weekly Earnings (blue line) and Statutory CEO pay (red line) both indexed to 100 in 2001. The data is also deflated using the Consumer Price Index, so reflects real growth.

I also use Average Weekly Total Earnings (which provides some measure of the shift towards part-time work) and a better indicator of the central tendency in the labour market.

Real Average Weekly Earnings Total Earnings (annualised) have grown by just 19.6 per cent since 2001 (up to 2016), while Statutory CEO Pay in Australia has grown by 33.6 per cent (up to 2016).

Of course, the CEO real pay exploded in the financial market frenzy before the crisis and by 2007 their real pay had risen by 77 per cent since 2001, compared to the average worker’s real wage rise of 11.2 per cent over the same period.

Since 2012, CEO real pay has risen by 1.7 per cent compared to real AWE 0.9 percent.

Between 2015 and 2016, CEO real pay rose by 2.1 per cent while real AWE rose by just 0.5 per cent.

The more recent period will see real earnings growth for average workers hovering around zero (if not negative) while CEO pay continues to growth in real terms.

Conclusion

There is a stream of research being published that demonstrates how fractured modern (financial) capitalism has become. In the post Second World War II period, the Cold War warriors in the West lampooned communism on the basis that the capitalist dream was spreading its rewards to the workers as well as to the owners of the capital.

The full employment consensus that emerged in that period, mediated by Social Democratic governments, achieved both productivity and real wage growth and more or less comprehensive Welfare States, which raised the material living standards of workers rapidly. At least, in the developed world.

There was also a sense that the regulative environment and cultural overtones had kept the capitalist class in check in terms of their share of the pie.

Of course, there was also a sense that the exploitation of workers in poorer countries in Asia, Latin America, Africa and elsewhere was increasing to allow the West to satisfy the demands of more organised workers in the advanced nations for better living standards.

With the abandonment of the full employment consensus, variously, around the mid-1970s and beyond (depending on the nation), and the emergence of Monetarism and its micro-economic manifestation (privatisation, deregulation, etc), that lull in worker exploitation in the advanced nations came to an end.

Capital found a way to co-opt the state to work in its favour more fully and abandon its role as a mediator in the class conflict, which up until then, following the end of the War, had helped workers improve working conditions, pay levels, and provided social wage benefits in the form of public education, public health, public transport and all rest of it.

It’s interesting that the Left have bought the myth that the state is no longer relevant or has the capacity to influence national economies in the face of globalisation and global financial flows.

But the state never went away. It is still as important as it ever was. It is just now, that it openly works in the interests of capital rather than acts as the mediator.

This ongoing CEO salary binge, even though it is clearly now often at the expense of their own companies well-being, is a sign that capitalism is once again getting ahead of itself.

We saw it at the end of the 19th century, which provoked the rise of trade unions and broad social movements designed to force elected governments to act more broadly in terms of the interests that it served.

These movements led to the Social Democratic era in the West. The lesson was that workers will only take so much and when their material living standards are so threatened, they retaliate and will not remain passive.

At some point, this neo-liberal era will be brought to an end by some similar type of worker reorganisation and uprising. I hope it comes within my own lifetime.

Be the first to comment on "CEO pay trends in Australia are unjustifiable on any reasonable grounds"