Contributed by Joe Montero

The pronouncements coming form the Reserve Bank are somewhat muddled. True, there is valuable data, and this reveals part of the picture. But analysis is let down because everything is interpreted through the eyes of a political and economic bias.

According to this bias the economy more or less often functions well, and when it goes a little off course, a twitch here and a little push there, sets it all back in place. No other possibility is ever considered.

Much of what we hear concerns relatively short-term cycles. They last roughly a decade. There is a going up and then there is a going down, followed by another rise. This has been going on for centuries. Predictions about what will happen over the next few years are based on these cycles. The present one is no different.

Ignored is the reality that there are longer term cycles, and that these are ultimately much more important. We can consider today’s date in the framework of the shorter cycle or the long term cycle. The shorter one tells us that the ups and downs will continue. And in this vain, the Reserve Bank confidently predicts that there will be some change of fortunes within the next three years.

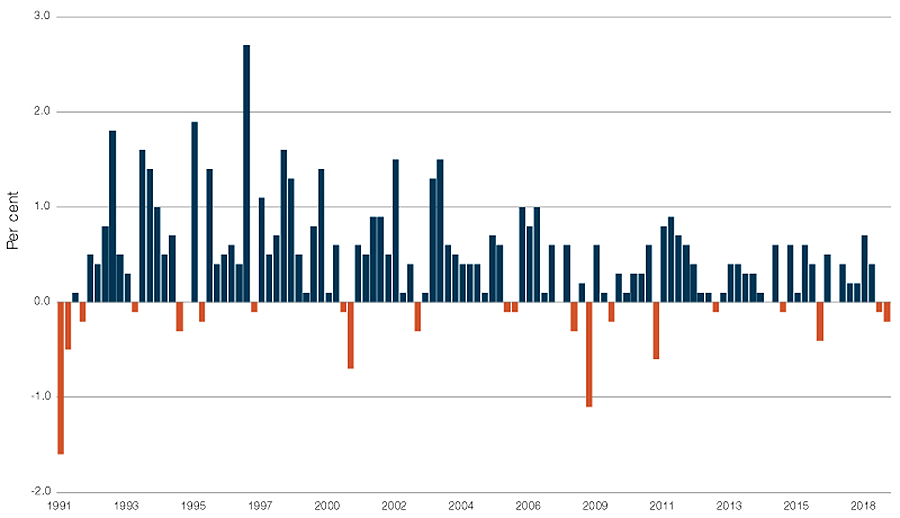

Source: Australian Bureau of Statistics (ABS): The graph clearly shows the two types of economic cycle. By only seeing the shorter term, the long term trajectory is overlooked.

Consider it from the long term cycle and the news is far less positive. They usually last about half a century. The current one is different though. It began with the post-World War Two boom, which petered out by 1967. It’s been downhill from there according to the long term trends. A series of events marked it. The debt crisis of the 1960’s ending in the mire of 1973, that threatened the global financial system. The stagflation of the following decade, the recession of the 1980’s, the crisis of 2008. And the present situation.

The above describes the global situation. So, it follows that there is a global aspect to Australia’s economic fortunes or misfortunes. But everything can’t be blamed on this. The continuum has played out in Australia in an Australian way.

These can be viewed as standalone events or as a continuum. The Reserve Bank insists on seeing these in the former sense and ignores the continuum.

Consider the same timescale. Australia emerged out of the war with a period of industrialisation, growth, and overall rising living standards. Manufacturing virtually went out the door. Stagflation hit, jobs went, and many of those remaining were transformed into insecure and underpaid work. Real wages began to fall. A debt crisis appeared and became worse. Now we have a worsening cost of living crisis.

None of these trends are sudden. All of them are part of the long term cycle. Their impact depends largely on how they are handled by the government and its authorities, business, and the rest of us.

Being only concerned with the short cycles, means that the deeper issues are ignored. This is tantamount to no action. The long-term cycle must be taken on to be effective. It isn’t because short-term interests stand in contradiction to the longer-term interests of the economy and society. The main one is the bottom line of the corporate sector.

This is getting harder to do. The long term cycle is bringing in greater instability and more uncertainty. Predictions are getting harder to make, and political expediency pushes government to cover up what doesn’t suit its immediate interests. The public is denied knowledge about what is going on.

Last year the Reserve Bank promised that the interest rate would peak at 3.6 percent. Now they are saying will go to 4.1 percent. It is the shorter-term cycle view. The truth is that they don’t really know. What happens will be decided by factors dictating the long-term cycle.

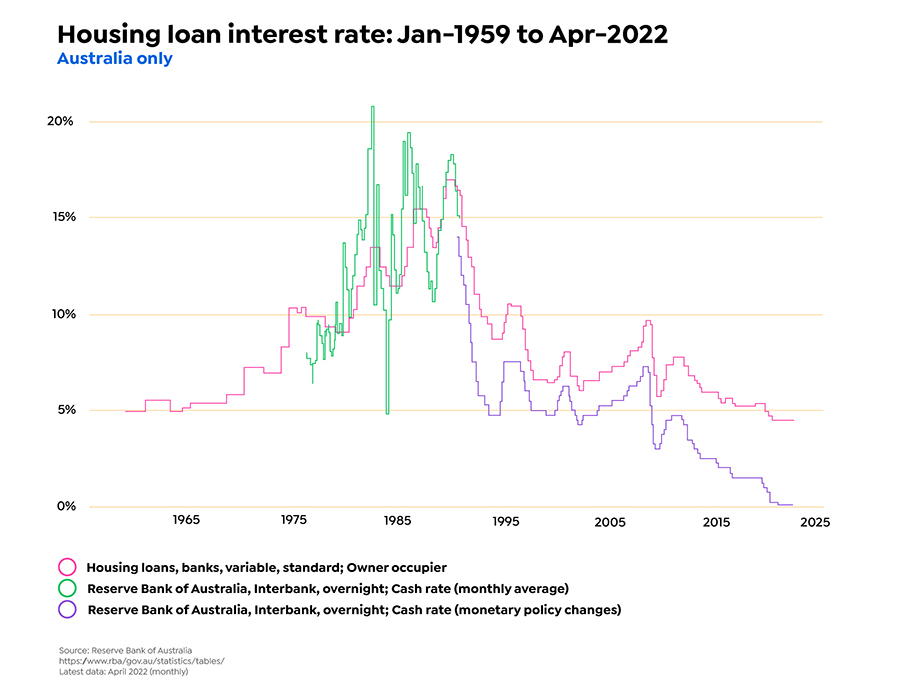

The graph shows the long term and the short term fluctuations around this. Note that the time from the mid 1970’s to the late 1960’s market the period of stagflation. It did not change the longer term trajectory of interest on housing loans, the overnight cash rate, or cash rate.

In its Statement on Monetary policy released last week, the Reserve Bank stuck to the short term, and in reality blamed the present situation on there being too low an unemployment rate, an economy that is over heated and forging ahead. The fall in consumer confidence, it seems, is blamed on the failure of the community to appreciate it is better off.

The political and economic bias is behind this.

Interest rates are being pushed up to dampen the economy.

According to the bias, this will cause more unemployment, and this will put downward pressure on wages. Investors will have more. They will invest this and create new jobs. The economy will grow, and wages will rise.

This is business as usual. The same policy has been applied over the decades of the existing cycle. It hasn’t work, just made matters worse, and the longer term trends keep on asserting themselves.

When you consider that the economy is growing less than 2 percent according to the GDP measure used, the performance is poor, whichever way you look at it. Add on discounts like changes in the ownership of assets causing inflated prices, and consider the real economy, the performance is even worse. Truth is, we don’t know whether Australia is moving to closer a precipice and risking falling over the edge.

How can Australia get around this?

A good place to start is to do something about the rising instability. The epicentre of this is the financial system. Its deregulation in the 1980’s made matters worse. It must be re-regulated, and opportunities to direct investment to where it is really needed must be created. The financial system should not exist to feed speculation and create unsustainable debt, at thee expense of growing the real economy.

This means going all out to develop advanced technologies, building the ability to produce, and doing so in a way that is both economically and environmentally sustainable. The private sector is not capable of doing this on its own. Public sector and community involvement are essential.

Sustainable growth depends on a healthy market, and this requires the of the community’s discretionary spending. It demands seriously tackling the cost of living crisis. The way to do this is for real wages to go up. Another is to supply better and cheaper government services.

This is affordable. If something was done to put an end to corporate tax evasion, which amounts to billions of dollars a year. This alone would raise a good part of the needed revenue.

Bias will prevent these changes being made. Australia will continue marching down the same road, lurching from crisis to crisis, and to wherever this takes us to. Unless the Australian community pushes back hard enough to take the alternative.

Be the first to comment on "The Reserve Bank is not telling us the whole story"