Contributed by Joe Montero

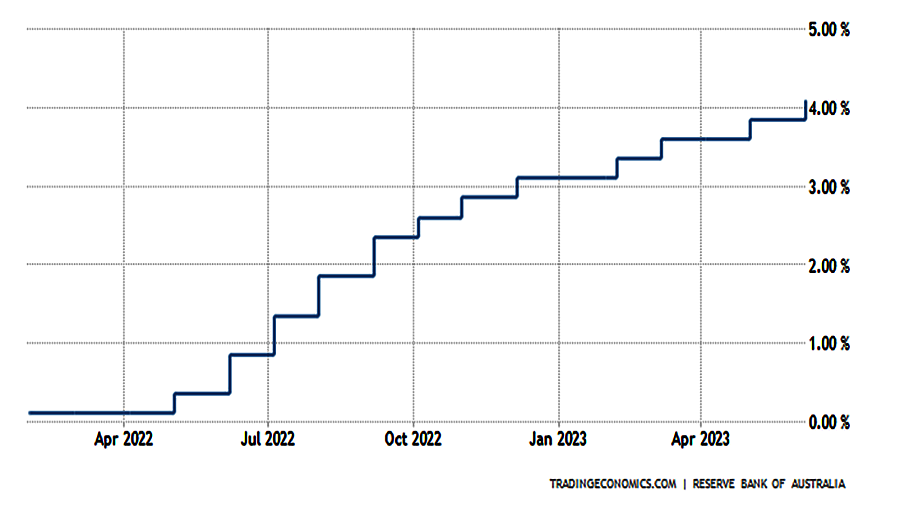

The Reserve Bank raised the interest rate yet again yesterday, and in doing so raised the ire of just about everyone. Yesterday its cash rate went up by another 25 basis points, taking the cumulative total to 4.1 percent.

According to the economic theory that has long been taken as gospel in countries like Australia, central banks shift the interest rate to maintain a balance in the economy between demand and supply. If this did work in real life, there would be no argument. Problems would quickly be fixed.

Those who persist with the above view, argue that the problem is that there is too much demand and real incomes must therefore be pushed down. This has been the approach taken by the reserve Bank, and the ongoing interest rate hikes have not overcome the persistent inflation.

Australia has seen a succession of interest rate rises since early 2022

What it has done, is to provide plenty of scope for the blame game. Shadow treasurer Angus Taylor says it is the fault of the budget. The Australian Chamber of Commerce and Industry blames it on wages being too high.

The Australian Council of Trade Unions (ACTU) has countered by using findings from research by the Australia Institute’s Centre for Future Work blames the interest rate rises on profit gouging by corporations. They are using monopoly power to raise prices above what the market would otherwise allow. Petrol and supermarket prices are two good examples of this practice.

This does translate into inflation. There is good reason to call it out.

It’s not the budget, because it was fairly neutral in terms of spending and will not have much effect either way. Wages continue to be almost stagnant, with minor increases well behind inflation. This is not the cause either.

Still, the problem is not only profit gouging. If we want to get down to the bottom of this, we must understand that inflation is all about the money supply. That is, how many dollars are in circulation and how fast they are moving in relation to the goods and services provided in the economy. If they move in in different directions or proportions, there is either inflation or deflation.

This operates within the fabric of the economy. The government and Reserve Bank don’t control it. All they can do is give it a small nudge in the preferred direction, and for a limited time. The underlying forces within will always eventually re-assert themselves.

If there is persistent inflation, it is the structure of the economy that is at fault. This is what is being overlooked in the present debate.

Inflation has kicked in and taken root because the economy is dysfunctional, and operating in a way where the money supply is outpacing what the economy is producing. This means that the value of this money is declining. In other words, it takes more of it to buy what we need,

Using the Reserve Bank to raise the interest rate claws back some of the excess money in circulation, but not nearly enough to make a huge difference, especially in relation to the hardship it causes.

Image by Joe Benke

In any case, if clawing Back the money supply is necessary, it would be much more effective to close the massive scale of corporate tax evasion and use some of this to boost what the economy produces. The key would be to nurture new industries around the newest technologies and sustainability’ plus an extended program of infrastructure building to assist this.

We know that the market is not doing the job, and this means direct government involvement is necessary.

On top of this, the government can take action to ensure that a significant part of the money supply is directed towards where it is most needed. Taxation reform is part of this. The promised top end tax cut must not go ahead.

The government must set new priorities on what it spends on. Building the economy and sharing the rewards fairly must be at the top of the list.

Raising wages and fixed incomes provided by Centrelink would help to quash the misallocation of money into problem investment areas, be spirited away overseas, and counter speculative investment. It would mean an expanded market for the goods and services that Australia produces.

A recovery plan on these principles will do much more to set the economy on a good path.

WHAT A SOUND ARGUMENT!