The Pen has published a number of articles in its short existence, which put forward the proposition that the excessive transformation of Australia into a services economy, led by the financial sector, has not been good. The following article from Michael Janda (ABC 18 June 2015) was sent to us and remains just as relevant today. It deals with two important aspects of the problem, the impact on economic growth and inequality. The article has been republished, to encourage ongoing debate and the search for an answer.

A new OECD report finds that the bloated banking systems in most developed countries are sucking growth out of their economies as well as increasing inequality.

The Organisation for Economic Cooperation and Development, a Paris-based think tank of advanced economies, found that the deregulation of finance over the past 30 years has probably stunted, not boosted, economic growth.

“The empirical analysis documents a link from financial deregulation, measured by an aggregate indicator, to credit expansion and slower growth,” the report found.

“The data indicate that credit intermediaries may have developed in most OECD countries to a point where further expansion is at the margin associated with slower long-term economic growth and greater economic inequality.”

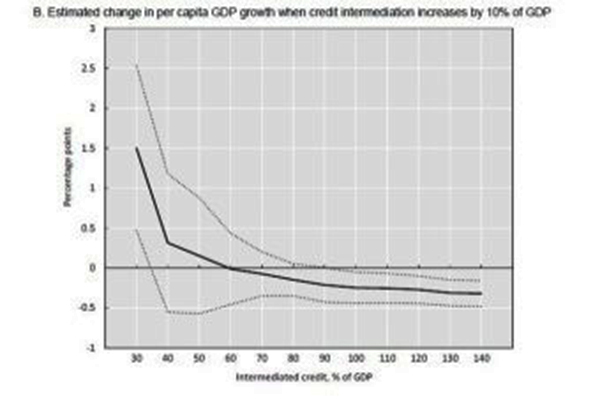

PHOTO: The effect of financial sector size on economic growth (OECD)

The report finds that an expansion in lending boosts economies up to a point, but when loans exceed around 60 per cent of gross domestic product (a key measure of an economy’s output) then further lending actually dents long-term growth.

“An increase from 100 to 110 per cent of GDP is linked to a 0.25 percentage point reduction in economic growth,” the OECD observed.

According to the latest Reserve Bank data, released earlier this month, Australia’s credit to nominal GDP ratio is above 140 per cent, putting it off the scale of the OECD’s chart.

That implies that the nation loses about a third of a percentage point of economic growth due to its bloated banking sector and excessive debt levels.

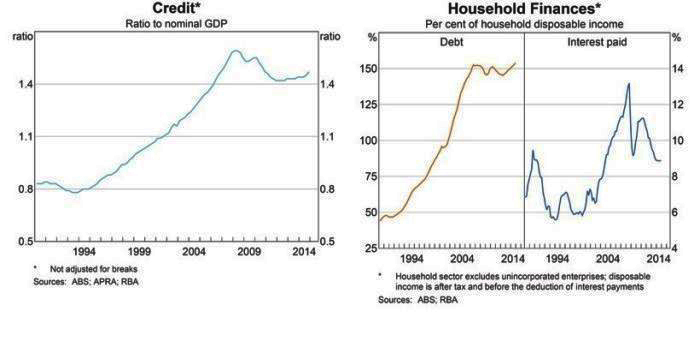

There is even worse news for Australia, where it is a surge in lending to households that has driven credit higher.

PHOTO: Australia’s credit to GDP and household debt to income ratios (RBA)

“The data show that households’ borrowing has a negative marginal link with growth that is twice as large as firms’,” the report noted.

That means Australia could be losing even more economic growth due to the banking system’s overwhelming reliance on home loans.

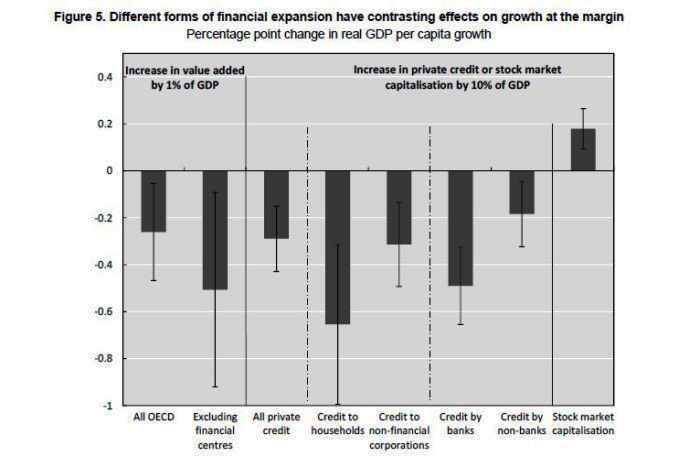

PHOTO: Lending expansion to households slows growth more (OECD)

The OECD report finds that it would improve growth for companies to rely more heavily on equity raised through share markets rather than debt.

“Causality appears to be running from more intermediated credit to slower growth and from larger

stock markets to higher growth,” it noted.

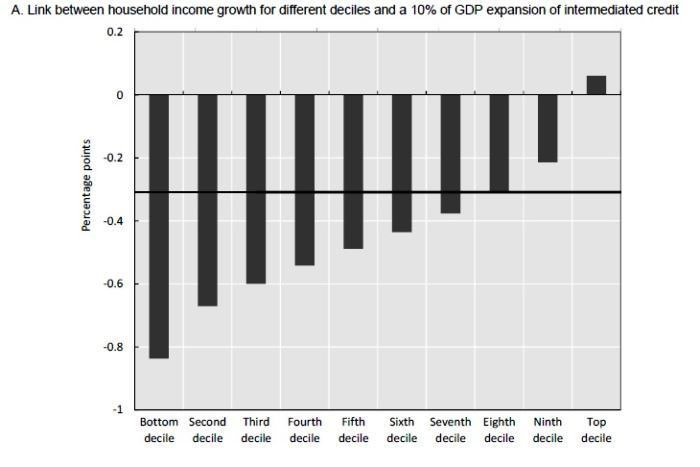

Financial sector growth increases income inequality

PHOTO: Expansion of credit makes most households poorer (OECD)

Aside from denting growth, the OECD has found that the massive growth of financial sectors in developed nations over recent decades has contributed to rising inequality.

“The links of more credit intermediation or stock market financing with greater income inequality are

established after taking into account a wide range of factors,” it noted.

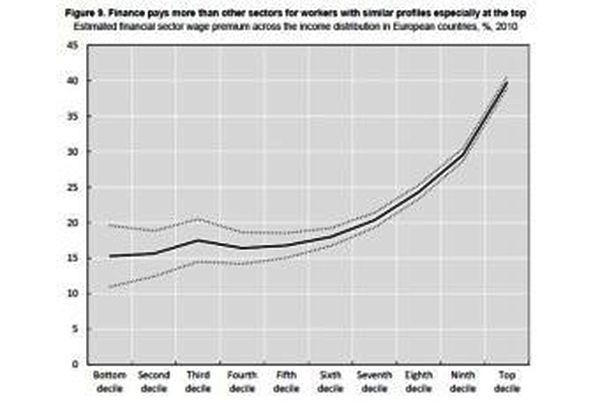

PHOTO: Financial sector staff earn more than equivalent people in other industries (OECD)

Financial sector workers have been found to earn a premium over workers in other industries with similar levels of education and experience.

That disparity is also believed to be one of the reasons why a larger financial sector actually inhibits economic growth.

“High wages can draw the most talented workers into the financial sector where they may not contribute as much to economic growth as compared to jobs in sectors with greater potential for productive innovation,” the OECD report hypothesised.

More regulation, demergers and a GST on banking

In response to these findings, the OECD suggests a range of possible policy responses, many of which align with the recommendations of David Murray’s recent Financial System Inquiry.

“The particularly strong negative association between increases in bank lending and economic growth underscores the benefits of reducing explicit and implicit subsidies to the banking sector,” the OECD said.

One way to do that is to ensure that no institutions are “too-big-to-fail” and therefore that none require explicit or implicit government guarantees.

“One way of ending too-big-to-fail would be to break up financial institutions into sufficiently smaller entities,” the policy think tank recommended.

The OECD is also concerned about policies that encourage banks to engage in more mortgage lending to households and less business lending.

In Australia, one of the key policies that does that is the allowance of the major banks to use their own modelling to rate the risk of home loan defaults and therefore how much money they need to set aside to cover potential losses.

The steep discounts the major banks have given themselves on the risk of residential mortgages have significantly increased the attractiveness and profitability of home lending compared to other loans, an area Mr Murray wants rolled back.

Negative gearing and capital gains tax discounts, including the exemption on the family home, might also be in the OECD’s sights given this comment: “There is scope for reform to make sure that tax provisions and regulations treat all kinds of lending on an equal footing, without encouraging the concentration of loans in

housing.”

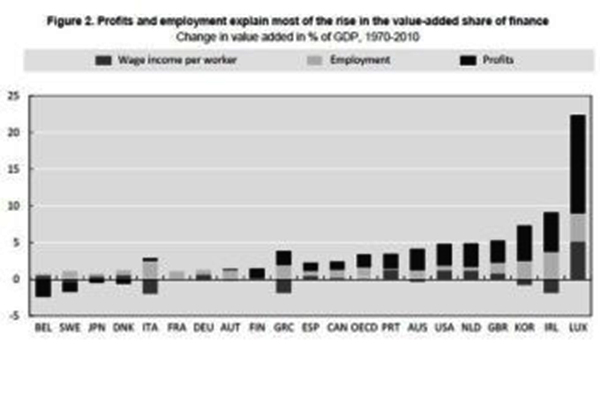

PHOTO: Rise in profits and staff drive growth in finance sector (OECD)

The OECD has also given a strong endorsement to the kinds of ‘macroprudential’ measures that New Zealand is taking to slow home lending growth and take heat out of a roaring Auckland property market.

These are stricter than the softly-softly behind the scenes measures that Australia’s banking regulator APRA has been tentatively taking over the past six months.

“The link of more credit intermediation with slower and more unequal income growth highlights the benefits of using macroprudential measures such as debt service-to-income ratios to curb credit booms,” the OECD argued.

“The long-term benefits for income equality that can be expected from such macroprudential measures have to be kept in mind when considering that, in the short term, they may make access to credit and property more difficult for low or middle income earners.”

With debate raging on possibly extending Australia’s GST, the OECD suggests that applying it to deposits and loans might also be a good idea to discourage excessive borrowing.

“Extending value-added taxation to deposit-taking and lending would avoid favouring households over businesses in bank lending activities,” the report noted.

With a suggestion that banks be charged GST on payments to them, such as cash deposits and loan repayments, but that payments from banks, such as withdrawals and loan disbursements, see a GST refund.

Be the first to comment on "Financial sector expansion slows economic growth and widens inequality"