Contributed by Joe Montero

The latest survey by the Conversation should be of interest to everyone. It involved contributions from of leading forecasters in 25 Australian universities, thinktanks and financial institutions – among them economic modellers, former Treasury, International Monetary Fund and Reserve Bank officials, and a former member of the Reserve Bank board.

It is the unified view of the state of the Australian economy hat is the most noteworthy part. In short, the probability of a recession high.

The focus of the universities, think tanks, financial institutions, and the rest is on inflation and interest rates. No surprise here. Everyone knows they are a problem. We are all feel the impact on our lives.

But the forecast of a probable recession is about much more. It means a recognition that the economy is not growing and may even be shrinking. Predictions are that even if there is a small growth, it will be less than the increase in population.

Consideration should be given to the reality that official statistics are not accurate and tend to underestimate what is really going on. The reasons are that the methods used tend to be those that paint the best picture for the government.

Take inflation. A price index is used. It contains a basket of essential items for a household and their prices. What is included and whatever weight is given to each of these items matters. The cost of housing is underestimated, and high tech items like computers, mobile phones are excluded. These are just two examples that indicate the Index underestimates the real rate of inflation.

Economic growth is generally measured either by means of the money value of sales. This is called gross Domestic Product (GPD). But there is a problem with this. Financial transactions are considered parts of growth, when all they are is changing ownership of what already exists. There are also certain costs, like those resulting from environmental and social damage that aren’t included.

If these factors are brought into the calculation, the GDP measurement would show less economic growth.

This gives us a clue as to what is really going on. Finance in proportion to the rest of the economy has become far too big, and the largest part of this takes the form of debt. In turn, this debt takes two forms. Debt used to finance business and household debt.

When the first form of debt is directed to non-productive, speculative investment it takes from the productive economy, It’s harmful. When the second type means that households are trying to maintain their standard of living by borrowing, it causes another kind of harm.

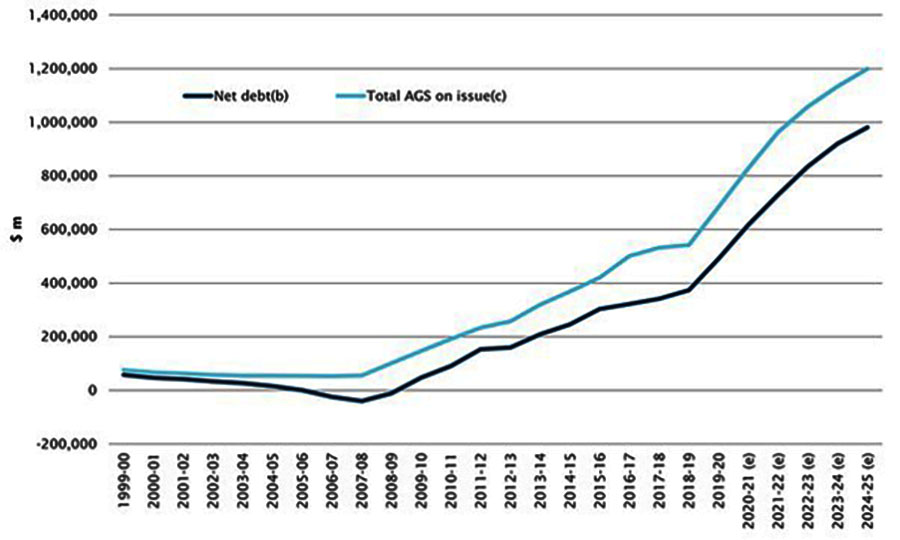

At the end of the last financial year, Australia’s net debt sat at a massive $963 billion at the end of the previous financial year. This is what was tabled at the time in the parliament as part of the government’s budget estimates. The present data showed that this was 45.1 percent of Gross Domestic Product (GDP). This debt was projected to increase to 50 percent in this coming financial year, with no sign of it going down again.

Rising debt was illustrated by the graph below, which was included in the government’s documents.

A nation’s ability to sustain debt becomes especially important in a situation like this. A combination of rising debt and a sputtering economy means a rising inability to sustain debt.

This has been downplayed by government and the bulk of economists. It doesn’t fit the politically opportunist narrative of happy days ahead.

More importantly, the reality has been papered over by the volume of transactions feeding the real estate bubble, the stock market transfer of shares, and the temporary, and now declining, prices for Australia’s fossil fuel and mineral exports.

When debt can no longer be serviced through real economic growth and the gap keeps on widening, by definition, financial transactions are outpacing the economy and have therefore become too big.

The Reserve Bank’s successive interest rate hikes recognise this. Well, sort of. The bank continues the mantra of blaming too much going to wages. But the interest rate hikes do admit that there is too much money in circulation. The fault is that the Reserve Bank points to the wrong cause.

It’s not hard to see that the real cause is bad investment in the creation of debt. If the intent is to take on the disease and not rely on snake oil solutions, the structural problems of investment in Australia’s economy would be admitted and changing this would be the priority.

Here are some suggestions.

Reduce the housing bubble through the provision of enough investment in public and social housing. This would result in an enormous difference to household debt.

Introduce a tax system that has the following legs. Income tax to be structured so that those with the highest incomes pay a higher proportion. Bring in a net profit tax for large companies, which is harder to avoid and works towards a more equal contribution. Impose a tax on business activities that contribute to harming the environment, and therefore imposes a further burden on Australia.

These new revenues can be used to solve the housing problem and build the economy creating the goods to meet the needs of people, and to do it in an environmentally and debt sustainable way.

None of this is possible without bringing in sufficient control over the finance economy. This must include regulations and penalties to ensure that investment does not centre on profit through the creation of debt and speculation. It must be directed to where it is most needed to meet the needs of society.

The excess money supply can be brought under control through these means. Interest rate hikes would be unnecessary. Jobs and wages would not be sacrificed. Big investors would contribute more. This is no disaster. They would still he able to generate a profit and potentially benefit from a healthier economy.

Greed, short-sightedness, and dogma are getting in the way. While this persists, Australia’s economy will continue to spiral downwards. There will be a point where ordinary Australians will insist on a more radical solution. This is the removal of those who now have the power in their hands.

Can you please check the accuracy of this and make appropriate corrections?

“At the end of the last financial year, Australia’s net debt sat at a massive $963 billion, and this is what was tabled at the time in the parliament as part of the government’s budget estimates. The data showed that this was 45.1 percent of Gross Domestic Product (GDP). This debt was projected to increase to 50 percent in this coming financial year, with no sign of it going down again.”

The level of net debt at the end of May, according to the Finance Department, was just $516.7 billion, which is lower than at any time since May 2020.

There has been no significant increase in net debt or gross debt since June 2022.

Thanks for pointing out the above. Rather than in fact, the error is in inaccurate explanation. The confusion is my fault. This has been corrected. The debt refers to the debt of Australia and not just government debt. Your figure of $516 billion refers to government debt. It also referred to the figure of the previous financial year. There has been no significant change here. The following figures rate to the current situation.