Contributed by Joe Montero

According to the Reserve Bank of Australia. Australian house prices are set to continue rising and are expected to go up by 10 percent this year. February recorded the biggest price rise for a moth in the last 17 years.

The rider is that this is assuming an end to the impact of Covid-19 and population growth going back to the pre-pandemic rate.

Goldman Sachs is a little more pessimistic and sees the price only going up by 5 percent.

The real estate industry believes this is a good thing. After all, it profits from it. But for those already facing a housing cost they already can’t afford, it’s a different story.

Economic forecasting agencies and government have long tried to pass off the housing bubble as indicators of rising wealth and economic growth. For instance, it is said that the expected further price increase will add a percentage point to Australia’s Gross Domestic Product (GDP).

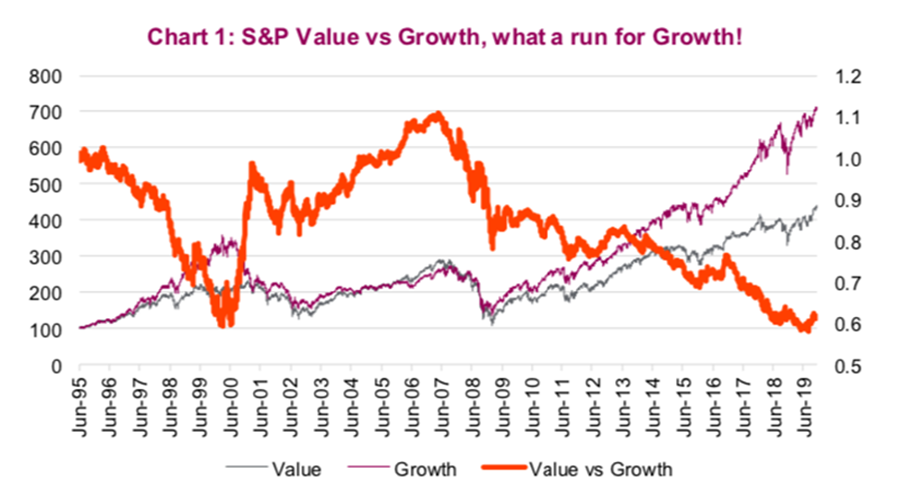

the above graph from Standard and Poor’s show the contrast between GDP growth and growth in value. It used to be that more detail was once published. This has stopped. Nevertheless, the difference is largely due to the rise of finance as a proportion of the economy, and the housing bubble is an important part of it.

How can price increases of what already exists, in themselves, add to GDP? Real growth is an increase in the quantity of what a society produces for itself, not how much it has to pay for it. Still, this is not how GDP is measured, although it should be.

House prices have been rising because the economy is not doing well. When the return of investing in other pursuits falls, investors with the means tend towards putting their money in bricks and mortar. History has shown this.

We can also see that the big buyers are not mums and dads. It is part of the corporate world that is becoming the new owner and landlord of homes.

A faltering economy has led to a plunge in the interest rate, making borrowing extremely cheap. The housing bubble is being funded by an explosion of debt.

The corporate shift into the housing market was a feature of recent years and important in fuelling the bubble. But these investors have pulled away a little over the last two years. But it keeps on going thanks to some of the other factors.

The generous negative gearing provisions that use taxpayers’ money to cover losses on rental properties is one of them. It is often more profitable to leave them empty than cover the costs of having them occupied. This creates an artificial shortage of available homes for rent.

Add that existing benefits allow corporate tax avoidance in other areas. Real estate becomes a type of money laundering operation. One is the Capital Gains Tax exemption. Other measures allow some creative accountancy, making an investment look like a cost, and therefore tax deductible.

Many have written volumes on these issues. Not that is has had an impact on those in position to do something about it.

The damage to the economy is considerable. The most obvious, is that it robs investment from here it’s really needed, and therefore, accelerates a decline in other industries. It also restricts the capacity of Australians to spend on other things. The rise in relative poverty impacts through the whole economy.

Unless it is checked, the bubble will burst sooner or later. Much better if something is done to bring it down in a managed and smoother way. The government could implement several practical measures.

Incrementally reduce negative gearing and the tax advantages going to corporate owners and establish rent control that established a maximum allowable rent. To make a real difference, this must be complemented with a big enough program to build affordable housing. The only way to do this is through public provision and legal recognition of adequate and affordable housing as a human right.

Be the first to comment on "Measures to bring down the cost of housing are needed"