Contributed by Joe Montero

Australia’s inflation rate is rising and set to rise further still. In the first three months of this year, it rose 5.1 percent, according to Jim Chalmers, the Treasurer of the newly elected Labor government. He has suggested that further interest rate rises are on the horizon. The Reserve Bank has not made back top back interest rises for 12 years. The last time was soon after the Global Financial Crisis. Something is in the air.

“It’s now really clear that the inflation challenge that Australians are facing is worse,” Chalmers told News Corp interview.

This is bad news for borrowers, a higher cost of living for Australian citizens, which makes the effort to make ends meet each week more difficult. And it is bad news for an economy already far from healthy. The only ones to benefit will be lenders enjoying a bigger return from the interest paid t them.

The problem is bad enough to make the new government announce it will deliver an economic statement next month. This is effectively a mini-budget.

Blame has been put on the war in Ukraine pushing up global price of power and goods. We have certainly felt the price at the petrol bowser. Ukraine has had an effect.

But it is far from the only cause and not even the most important one. To understand this, we must know what inflation is. In a nutshell, there is inflation when there is an imbalance between what we buy and the quantity of money in circulation. Since more money is chasing the same quantity of what we buy, prices go up. We must know what is causing this imbalance to understand the inflation Australia is facing.

There are two parts to the problem. A part of the inflationary pressure is imported, not so much because of Ukraine, but because global investment has dropped markedly.

In 2020 alone, it dropped by a whopping 35 percent, according to the UN Conference on Trade and Development (UNCTAD). There was not much of a recovery in 2021, and this year, the deterioration has continued.

A considerable amount of current global investment is devoted to the China initiated Belt and Road Initiative (BRI), and concentrating on cooperation in infrastructure development and green and digital projects.

And this is only part of it.

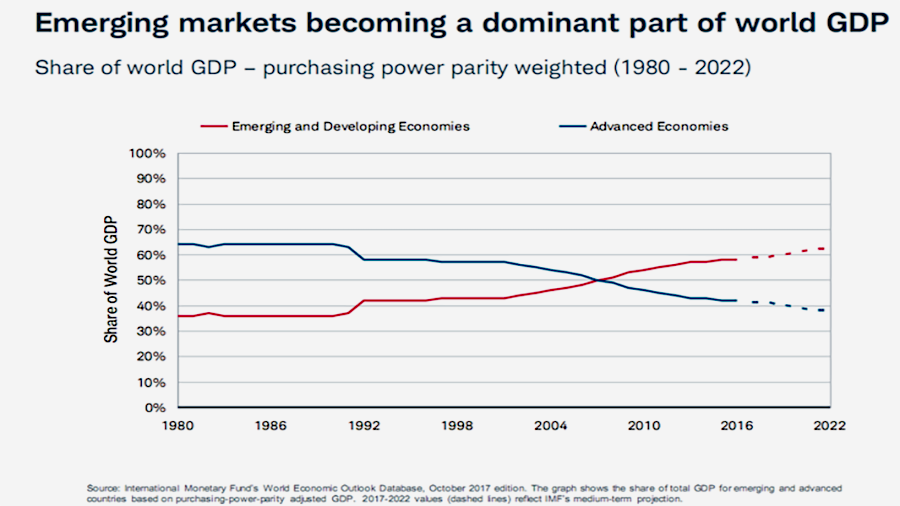

The following graph shows that emerging economies, particularly China, became the dominant part of global GDP since the Global Financial crisis of 2008-9 2017 and their lead has continued to extend.

Add that China holds more than $3 trillion in foreign reserves, and two thirds are in United States dollars. This is by far the biggest holding in the world, three times that of Japan the second-place getter.

By imposing trade and investment restrictions on China and non-cooperation with the BRI, western nations closely allied to the United States, including Australia, have hurt themselves by cutting down opportunities for investment, precisely when they are losing ground.

This combined with the restrictions imposed on trade and investment with China means the flow of investment slowed. Last year the US Federal reserve offered bonds at a higher dividend to encourage investment flow into the domestic economy. This kept the exchange value of the greenback up at the beginning of this year.

But the lack of growth in global trade resulting form already existing structural blockages and made worse by the pandemic and Ukraine, together with the sluggish flow of investment, is causing prices to rise.

Washington is now contemplating lifting of some of the sanctions on China to import goods and investment, to counter the pressure to push up domestic inflation.

The global environment is affecting Australia.

There is the addition of domestic factors. The biggest raiser of prices in Australia is the cost of buying or renting a home. The second is the cost of food and non-alcoholic beverages. The third is the cost of transport. Prices for necessities (non-discretionary spending) increased at twice the rate of non-essentials, meaning that they have impacted most on those dependent on wages and Centrelink payments.

The gap between wages and costs

Rising housing and food costs are partly the result of a continuing speculative bubble and supply issues due to fire, flood, and logistical problems, and they are partly the result of an underperforming domestic economy, not merely pressure form the global economy.

In trading with the rest of the world, Australia’s current account balance fell from $13.2 billion last year to $7.5 billion this year. This has had a major effect on income derived from Australia’s international trade. The net value of goods and services fell by $0.9 billion. But it has been the $15.2 billion fall in capital imports that has caused most of the hurt. A substantial $183 billion flowed out of Australia last year. And part of this was payments of dividends to overseas shareholders.

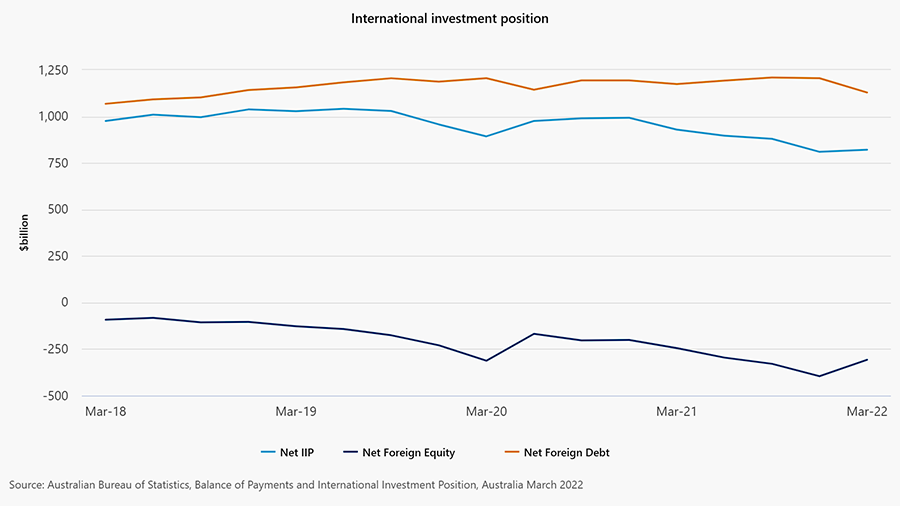

Foreign investment into Australia has remained flat this year, as the graph below shows. The foreign equity part, that is, investment is shares has been negative, which means de-investment.

How is all this affecting inflation?

It was said that inflation happens when there is an imbalance between goods and services and money circulating in the economy. The market for goods and services has not been able to grow as much as it could have if the real wages share of national income had not been kept down, there had not been supply shortages, and imports had not fallen.

Capital outflow has reduced the money supply by a proportionally bigger margin than the market has failed to grow. This puts pressure on the interest rate to rise. The fall in the money supply in the Australian economy, although not huge at present, is nevertheless enough to have an impact.

The Reserve Bank is manipulating the short-term interest rate to increase investment in the Australian economy. There is a lack of internally. It has risen by a mere 0.3 percent this year, even after the decline brought about be Covid. Investors are attracted by higher interest rates, and the Reserve Bank hopes that foreign investors will be enticed by the prospect of a greater return.

The Reserve Banks increasing of interest rates won’t work. There are other factors influencing the investors,’ and a big one is the expectation of how the economy they are investing in is expected to perform, relative to alternative opportunities available to them.

This highlights the need to pay attention to the core problem of how the Australian economy is really performing, and this means addressing the forces pushing it in the direction that it is going. It would pay to re-examine Australia’s foreign trading relations to link into where there is growth, instead of where there is stagnation.

Be the first to comment on "Australia’s inflation rate is rising and why this is happening?"