Contributed by Joe Montero

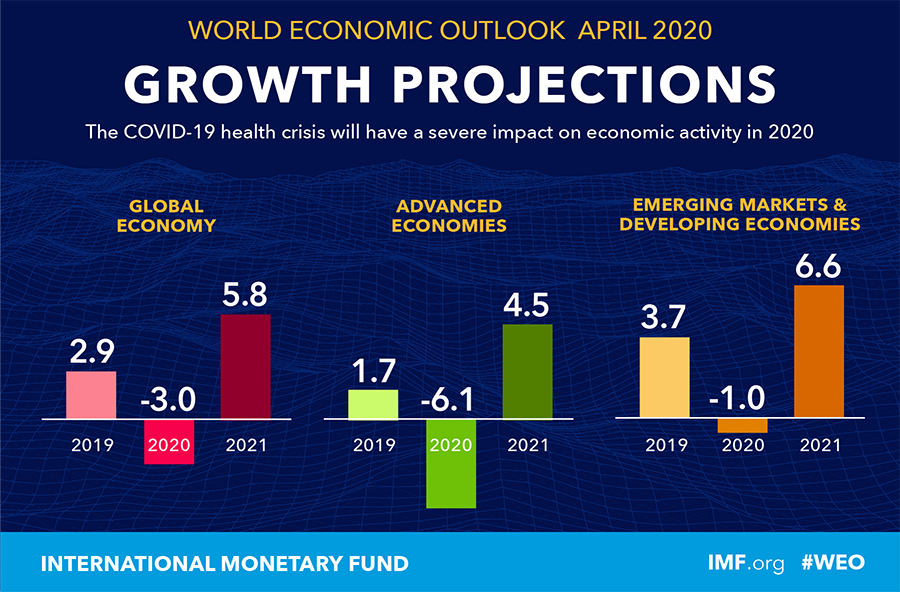

The International monetary fund (IMF) isn’t hiding its fears over the economic impact of the COVID-19 outbreak. A little over a week ago, it predicted that the global economy will contract by 3 percent this year. This pessimistic forecast was made public in the IMF’s latest World Economic Outlook.

The IMF also made it clear that the world faced the worst depression since the 1930’s, and that three quarters of the global workforce faced at least their workplaces being shut down for a period.

IMF’s World Economic Outlook, April 2020

Video from the IMF

The projection of possible growth in 2021 shown above, is based on the assumption that nations take on the IMF’s recommended rescue action, and even more importantly, the assumption that a big growth in the Chinese economy will hold up the global economy. It tends to hide underlying problems facing other economies. Thery can worsen and pull everything down.

This prediction was made just before the Spring meeting of the IMF and World Bank. They which re-affirmed the uncertain outlook.

IMF Economic Counselor Gita Gopinath wrote in the report: “It is very likely that this year the global economy will experience its worst recession since the Great Depression, surpassing that seen during the global financial crisis a decade ago.”

The data shoes that the advanced economies are the worst hit, as is shown in the graph below. They also have the resources to bounce back more easily.

Don’t assume that everything will be alright. Charity organisation Oxfam warned that the economic fallout from the spread of Covid-19, could force more than half a billion more people into poverty, taking the total to half the world’s population of 7.8 billion human beings.

In the United States alone, 16 million are now without a job. Up 6.6 million since the outbreak begun. Europe and every other continent have also been hit.

The International Labour Organization (ILO), a United Nations agency, warned that in terms of the loss of jobs, this is the most severe crisis since World War Two. And the Organisation for Economic Co-operation and Development (OECD) has made it clear that a recovery could take years.

Australia’s economy would be one of the worst hit in the Asian region, the IMF report warned.

One reason is the degree of dependency on foreign trade, which is expected to decline by 11 percent this year. A worsening economy and job losses, on the back of an already depressed jobs market, could be enough to burst the housing bubble and cause property prices to plummet.

Australia is highly dependent on foreign investment and therefore particularly vulnerable to shocks in the global financial market, which disrupt the flow of investment. Like changes to government expenditure, changes to this flow of investment will have a multiplier effect on the whole economy.

The Multiplier Effect

Video You Will Love Economics

The IMF’s and the World Bank’s answer to the threat, is for government to spend on the economy. Primarily on the health system in dealing with the pandemic in the immediate sense. There is an implication. More should be spend on infrastructure building.

But then, and more importantly according to both agencies, the ongoing functioning of the banks must be guaranteed, by providing a sufficient money supply (reserves). In other words, the government must be prepared to hand over money to protect the banks.

This is not going to win universal acclaim. Free market diehards will bulk at the idea of government intervention. Those who are for it, may be asking a very important. Where is the revenue for this going to come from? No answer has been given.

Unless there is a new source of revenue, it will have to come though cutting expenditure somewhere else, and this defeats the purpose of government intervention. Increasing net spending is the condition for any stimulus to have a chance of working.

If cuts leave the bulk of consumers worse off, the market is going to be contracted rather than simulated. It’s a dead end.

The revenue problem must be answered. Part of the answer could be to spend less to shore up the banks and use existing resources more efficiently, and in ways that raise the disposable income of the majority of consumers.

This could be achieved by lowering the cost of government services and building more affordable housing, for example: Health and education costs could be reduced. Other measures could be increasing Centrelink payments permanently and lowering the taxation rate for average and below incomes.

A minimum guaranteed income for all could be assured, jobs protected, limits set on rents and charges for utilities. Public transport charges could be reduced.

These would increase disposable income to be spent on other things, stimulate the economy, and even provide more business for the banks.

It should also be recognised that on their own, these stimulus measures will not resolve the cause of the economic decline. Nor will it provide total protection against sudden shock. But at least it will make the hurt s lot less and provide a better foundation for abetter tomorrow.

A big problem is that the existing revenue base will not be sufficient to cover the cost of a proper stimulus package. Revenue must be raised to cover it, and done so, from where it hurts the least, and not pull down consumption.

There is no way to avoid the necessity to finally take on the corporate tax avoidance and money laundering industry. The veil of secrecy makes it hard to estimate what this is in dollar terms. Nevertheless, the Panama Papers released by WikiLeaks in 2018, proved that the scale is massive. It is known that the 200 biggest companies operating in Australia pay less than 10 percent tax. Many pay no tax at all.

Calculated from the Australian Taxation office figures, the biggest companies paid only $14 billion out of $1.5 trillion in gross income for the 2014-15 financial year and revealed in 2017; meaning they avoided paying a substantial amount.

Measured by earnings before tax, which deducts legitimate operating expenses, would still leave due a sizeable proportion of the $500,000 billion under the company tax rate of the time.

Erring on the side of caution, just say, this leaves at least $100 billion a year in lost tax revenue. Recovering this would go a long way to pay for a worthwhile stimulus package.

Back to the banks. If the situation proves to be so bad, that there is no other choice but to help the banks so they don’t go under, this should be conditional on being in the form of short-term loans, or alternatively, the buying of voting shares in the bank.

After all, this is how the market is supposed to operate. And when it is ultimately the taxpayer wearing the burden, the taxpayer can claim the right to share in the benefits as well as the costs. Profit accumulated by the bank can be used for the whole community.

If the diehard defenders of the market don’t like this, then they should totally accept its operation of the market and oppose any form of government support. It is hypocritical to do otherwise.

The wisest course is to accept the reality and plan for a better future.

Be the first to comment on "The IMF predicts a possible global and Australian contraction on the scale of the Great Depression"