Contributed by Joe Montero

If we believe the political hype, the world is bouncing back nicely from the Covid-19 disaster, and this includes Australia.

Unemployment is said to be going down. It is said that the numbers say so. This covers up, of course, that a large part of this is the rise of casual and part time work to replace former full time and permanent jobs.

In most countries, including Australia, the impact has been cushioned by increased support spending by government. This has not only made lives easier than they would otherwise have been. Stimulus spending has held spending and therefore the economy.

This is all good. But it doesn’t change that the underlying problems are still there. History has shown that when these go unresolved and fester, the effect is first seen in the world of finance. All of its parts start to wobble.

The last couple of weeks have seen increasing turmoil in shares, government bonds. There is even increasing nervousness over the stability of currencies and interest rates shifting up form near zero. The price of gold is moving in the opposite direction and the price of oil falling.

What does this mean? It may not mean an imminent collapse. Who knows what’s around the corner? It does, however, mean that the engine of the global economy is running rough.

Much of the debate is currently on whether the problem is government spending and whether it needs to be reined in. Big spending without a corresponding lift in the economy will cause problems. An oversupply of money circulating will cause problems. Nevertheless, the real problem is why is the economy not lifting.

The global economy is largely being held up by the success of China. This is indisputable. It continues a trajectory of around 7.9 percent growth a year. The other major economies are moving in the other direction. The world Bank expected overall growth to by 4 percent over 2021 in January. The United Nations upped this to 4.7 percent. But most of this is covered by the restart after last year’s lockdown and plunge in economic activity. It is not real growth.

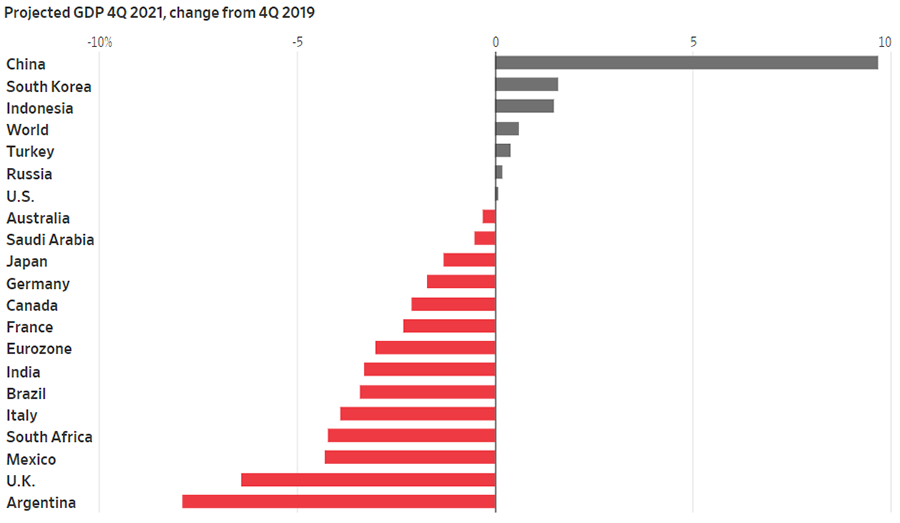

Chart from Sky View December 2020: The above projections have not changed substantially this year

Imagine where the global economy would be, if the world’s second largest economy were not doing so well.

There is clearly a serious problem and its epicentre is in the developed western nations, especially the United States. Australia is included.

The money paid out on U.S, government (Treasury) bonds has risen to a record level. The 10-year yields hit 1.75 percent and the 30-year yields went past 2.5 percent. This happens when major investors become nervous about putting their money in the share and other markets. From their point of view, these bonds provide government guaranteed protection against loss. Profits (yields) are guaranteed.

The volatility in the share market Nasdaq 100 Index, which dropped 3.1 percent last week, shows the nervousness around it. Crude oil is another buffer, used as a futures commodity. It is bought to be resold at a future higher price when there is an expectation of increased demand. The fall in its price, especially if it turns out to be prolonged, indicates falling confidence in the economy.

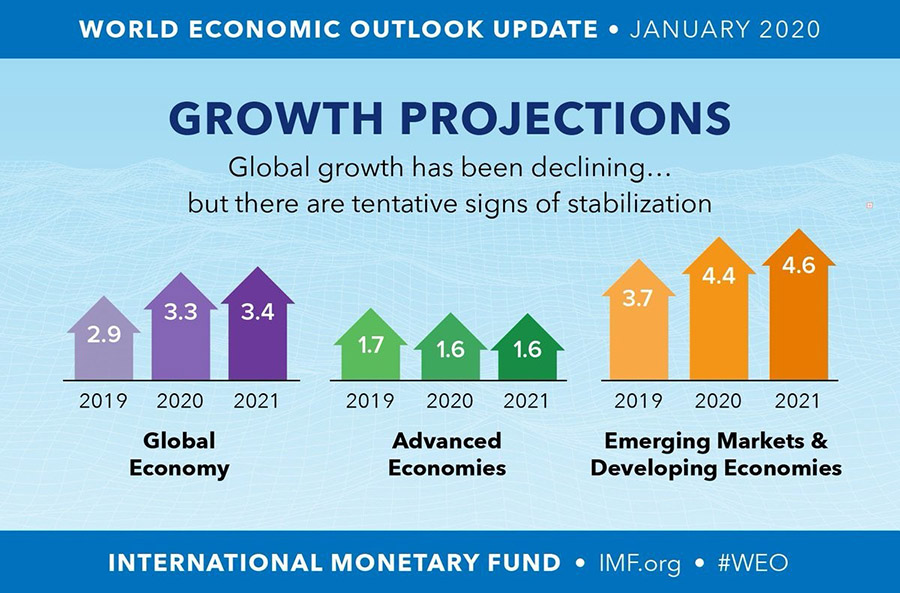

The chart below from the IMF tells us that the global economy was already performing poorly before the pandemic and is expected to continue to do so. Most of the growth that does occur will be from newly emerging economies.

Money collected by government from the sale of bonds is being used by government to finance incurred by stimulus spending through the creation of debt. Damaged is caused when this leads to an excessive money supply. The value of money falls and the prices of what we buy go up. This is inflation. It is bad when it causes the harmful allocation of resources and shrinks effective consumption.

There is the added potential to create debt that may not be able to be paid in the future.

One answer being demanded from some quarters deal with the money supply problem is for government to cut back on spending as quickly as possible. This would decrease the quantity of excess money in circulation. It would also pull away a necessary driving force to kick start the real economy. This is not the answer.

The problem lies in failure to target investment to where it’s needed. The major market failure to resolve this means that the only solution is a public sector led recovery based on a plan for national economic reconstruction around clear objectives.

The funds for this should not be raised through the sale of bonds. It should be raised through the taxation system. This would have two positive effects. It would neutralise the problem of an excess money supply through re-allocation rather than increasing quantity.

If taxation reform is based on lifting corporate taxation and putting an end to the massive tax evasion industry, it would channel misused investment capital to useful purposes, such as increasing needed infrastructure, seeding new industries. It can be used to lift the capacity of the population to spend, through the provision of services, creating jobs, and raising incomes.

This may not cure the whole problem. After all, it’s based on how the economy is organised to generates the main benefit for only a few. Changing this requires a democratic economy, where all of us have a voice.

Ditching the old methods might just help to shed a light on what is possible.

Be the first to comment on "Something is seriously wrong with the global economy"